Data Analysis: Australia's debt market

Australia’s debt market remains largely dominated by the big four Australian banks – Australia & New Zealand Banking Group, Commonwealth Bank of Australia, National Australia Bank and Westpac – although there are some signs that international lenders, traditionally content to club with Australian banks, are starting to rival their domestic counterparts on deals.

The A$5.9 billion ($4.1 billion) project financing for the Hastings-led consortium’s acquisition of the 99-year lease of New South Wales electricity distribution company TransGrid, which closed last month, was unusual insofar as the sponsors were able to raise such a large debt amount without all of the Australian banks participating on the deal.

Earlier in the year, Neoen, John Laing and Megawatt Capital closed a A$248.8 million 19.5-year financing with KfW-IPEX and Societe Generale, which was the first offshore financing in Australia for five years, according to data from IJGlobal. The push from international lenders into Australia has started to put pressure on the pricing and tenor banks are willing to offer as borrowers gain more leverage.

Data from IJGlobal shows that the average tenor for project finance deals in Australia over the last five years has been on a steady upward trajectory. Having plateaued at around three years between 2011 and 2012 the average tenor on deals for the last three years has ranged between around five and six years as international banks have started to disrupt Australia’s mini-perm market.

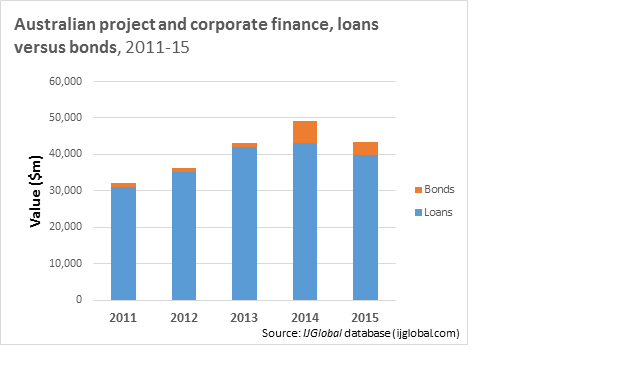

Data from IJGlobal also shows that there are signs borrowers are increasingly seeking to tap alternative sources of funding to bank debt for financing projects. The cumulative total for bond issuance last year exceeded $3 billion. This was the second year in a row it had done so having peaked at $5.9 billion in 2014 and only the second time it had done so since the onset of the financial crisis in 2008.

As interest rates begin to rise in the US the likelihood is that more borrowers will seek to issue bonds as the debt capital markets become more competitive. Australia’s currency swap markets also have enough depth too that borrowers will unlikely be put off by a weakening Australian dollar to issue in the US 144A markets.

It is common for Australian borrowers to bemoan the fact that tenors in Australia are shorter than those in Europe and the US and that the project market remains dominated by four banks that are able to dictate the terms on offer. This remains the case although there are some early signs as the shocks of the financial crisis start to fade that this is beginning to change.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.