Data Analysis: Limay and the Philippines’ power sector

For project bankers casting an eye around the Asia Pacific region for deals, many could be forgiven for ignoring the Philippines. The country is home to arguably Southeast Asia’s most developed independent power (IPP) market but opportunities for international lenders have been scarce in the last few years.

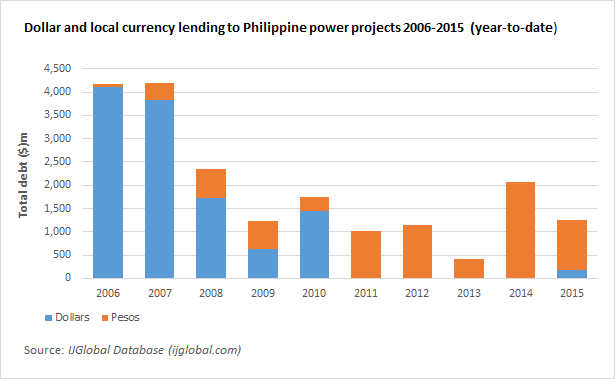

Data from IJGlobal shows that only one deal has closed in the past five years with any US dollar debt. This was the $315 million financing for the Burgos wind farm being developed by Energy Development Corporation. The debt included a US dollar tranche backed by Danish export credit agency (ECA) EKF.

This represents a complete reversal of a previous trend for international investment into the country. Foreign banks had been at the forefront of financing the privatisations of power plants mandated by the Power Sectors Assets and Liablities Management Corporation (PSALM) between 2006 and 2010.

As international banks have largely pulled back from the region in the wake of the global financial crisis, local banks have increasingly stepped up to fill the void left and the increasing competition in both tenor and pricing has meant that international banks have largely been frozen out of the market.

There is one deal that represents a curious anomaly though and that is the roughly $400 million financing for the Limay power project being developed by San Miguel. DBS, Mizuho and Standard Chartered have been appointed lead arrangers and are syndicating the debt to international lenders.

San Miguel, the Philippines’ largest IPP developer, is seeking to borrow in US dollars to hedge against foreign exchange movements. Exchange rates have started to become increasingly unfavourable for developers borrowing in pesos but saddled with payment obligations to offshore equipment suppliers.

If the syndication for Limay proves a success other large developers might follow suit. With local banks also said to be approaching their single borrower limit thresholds and the number of renewable projects, which lends itself to ECA financing, set to increase, Limay could be prove to be a watershed for international banks.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.