News+: Colombia's mega mission

In January, Colombia's national infrastructure agency ANI announced an ambitious P3 transport pipeline, one of the most ambitious investment programs launched yet, perhaps topped only by India’s. However, despite a new and improved PPP model, developers still face the immense challenge of financing the multi-billion dollar projects in a relatively small debt market.

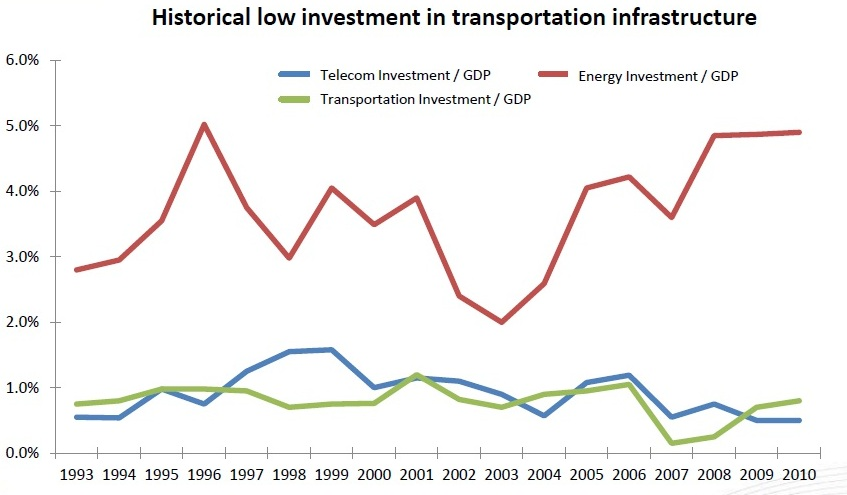

There has historically been little investment into transport in Colombia, which ranks low in the region for its road infrastructure. Indeed, transportation investment has been on average almost five times less than energy investment over the last couple of decades.

Source: Colombian National Infrastructure Agency (ANI)

In an exclusive interview with IJ News, Luis Fernando Andrade, President of the Colombian National Infrastructure Agency (ANI) revealed the proposed finance model for the US$26 billion highway megaproject. He describes the legal and institutional framework which has been adopted to underpin the investment into transport, in order to combat corruption and bureaucracy which has long since plagued public tender processes in the country. A law on public-private partnership (PPPs) was introduced in January 2012, which was accompanied by the inauguration of the National Infrastructure Agency (ANI) designed to build institutional capacity in the sector.

Currently under the spotlight is a highway renovation and extension program known as the “Fourth Generation of Highway Concessions” which includes the road megaproject, Autopistas de la Prosperidad.

Andrade admits that when he was designing the plan, he did not anticipate the cope of the program, being one of the largest of its kind, at US$26 billion in CAPEX, but reiterates that the program is validated by its “robust structure and improved and standardised contracts”.

One of the key improvements of the new adopted model, Andrade points out, is that “one, it’s transparent and two, it’s quick”. As the new law has established a critical prequalification stage, “only groups with sufficient financial strength and expertise can participate”.

“10 groups will qualify and the criteria for prequalification is very simple:

- Equity

- Leverage

- Experience

If they all qualify, there has to be a random process, because otherwise groups will often challenge one another’s prequalification”.

Due to the simplistic nature of the process, “it is essentially an economic contest which is easily evaluated”, explains Andrade. “There are no competitive dialogues and technical capability contests like in Europe”. Additionally, ANI will establish a range for qualifying bids, automatically eliminating very low bids that fall out of the range, which in the past has caused problems of contracts being renegotiated following the awarding of contracts, and ultimately delays in construction.

There will be a high-level committee established which reports to the President, “if bidders feel something shady is going on they can talk to the committee, which will then decide whether to take allegations further”, he adds, “there is a lot of disclosure in the process”, which is borrowed from the OECD's new methodology, to improve transparency in public biddings.

Colombia will be the first country to pilot the OECD’s new methodology.

The Fourth Generation of Highway Concessions involves 40 new toll road projects through which 8,100km of road will be built. The contracts include the design, renovation, construction and/or improvement of roads, operation, maintenance and finance. Each concession will last between 25 and 30 years.

Repayments will be made on an availability basis, through both tolls and government contributions (60:40). Concessionaires will also receive discounts related to availability, quality and service (capped at 10 per cent). All of which will be evaluated by an external auditor.

ANI will assume a series of risks to make the projects more attractive to developers, against factors such as, force majeure events, non-insurable events (e.g. natural disasters), land acquisition, social consultation, environmental licensing, traffic and utility works.

So far, the road projects have been met with major foreign interest, to be exact 172 EoIs from consortia across 70 countries in response to RFQs for nine roads, as previously reported by IJ News. The list of 20 consortia to manifest interest in the projects can be found in a previous report by IJ News here. Most but not all groups partnered with local construction companies.

However, while ANI has welcomed the warm reception to the road projects, it has faced some criticism surrounding the new PPP model. A source advising a group competing for the tender suggested to IJ News that the strong interest in the projects could be a product of more lax prerequisites for the concessions, and not solely an apparent enthusiasm for the improvement of Colombian infrastructure.

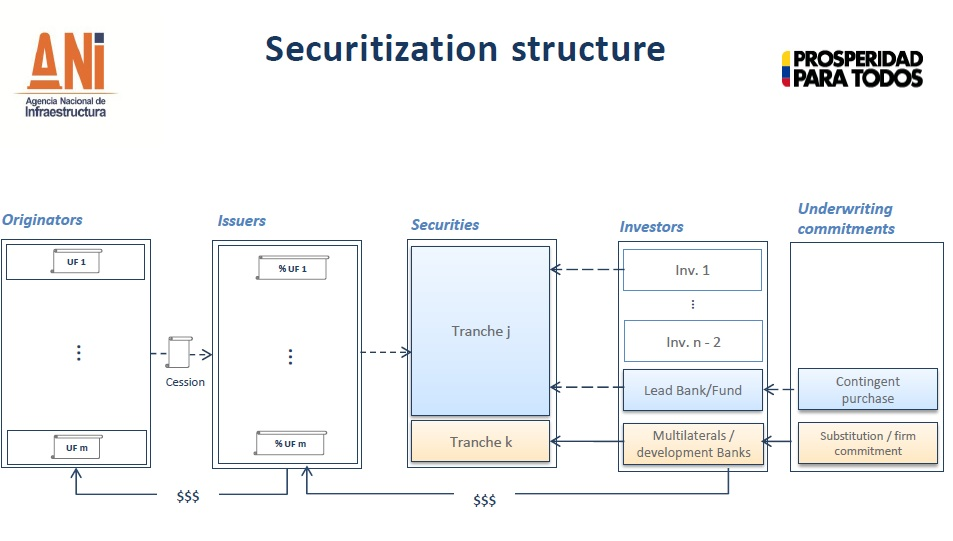

A broad finance structure

ANI has designed an innovative funding structure for its PPP pipeline. The agency estimates that the Fourth Generation of Highway Concessions will require around US$26 billion invested over the next eight years, according to an 80:20 debt to equity ratio. Each of the 40 projects requires around US$700 million capex, indicates Andrade.

In order to secure the financing, ANI is proposing a broad financing model, involving banks, multilaterals, development banks, private equity funds and institutional investors.

Institutional investors are key to the project funding model, Andrade emphasises and indicates that the government is prioritising their role in the financing aspect. It is seeking long-term investors for long-term repayment flows and demand risk coverage.

The agency is calling on infrastructure funds in the US and UK to compliment groups. Last week Andrade travelled to New York to meet with funds and discuss their potential involvement in the highway projects.

In order to entice pension funds and foreign investors and the like, ANI would like to issue securities at the beginning of projects, rather than at the end of the construction phase, Andrade explains, this would require elevated credit risk insurance.

Source: Colombian National Infrastructure Agency (ANI)

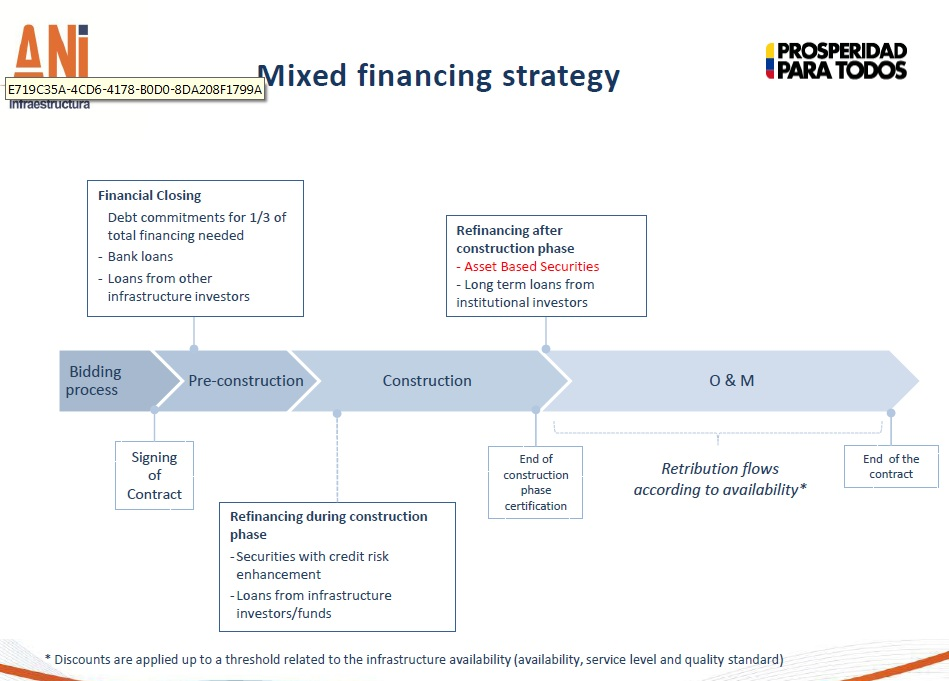

The bigger challenge, Andrade concedes, will be raising the vast amounts of debt in a relatively small local market. ANI estimates that local banks could finance around a third of this, at a push. The agency has looked to multilaterals such as the IFC, IDAB and CAF to bring confidence to the projects. Andrade indicated that he estimates these institutions could provide between US$1-2 billion to the megaproject.

Source: Colombian National Infrastructure Agency (ANI)

Andrade is confident the first nine projects brought to market will be financed, but admits the financing challenge will become tighter further down the line, as Colombian banks may be less inclined to participate again. The World Bank is advising Colombia in this project and Andrade assures “it will be figured out along the way”.

The capacity of the new PPP model still remains to be evaluated, perhaps until the first road is built, but there is a strong commitment to these projects from ANI and a sense from industry players that Colombian infrastructure is at a turning point.

The program is without doubt a huge undertaking and the financing challenge ought not to be underestimated, but if the projects arouse the interest of lenders to the extent they have drawn in foreign developers, the improved road infrastructure could transform the Colombian economy and pave the way for the flow of private investment into other crucial sectors.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.