Importing offshore wind experience

(Originally published in the Summer 2018 edition of IJGlobal)

Offshore wind projects are coming to the North American project finance market. Sites have been obtained, and importantly revenue-sources have been awarded to support major investments in several developments on the Northeastern seaboard. The next round of US offshore wind project finance could begin later this year or early next. A template for these deals is certain to be informed by the extensive experience among the European players.

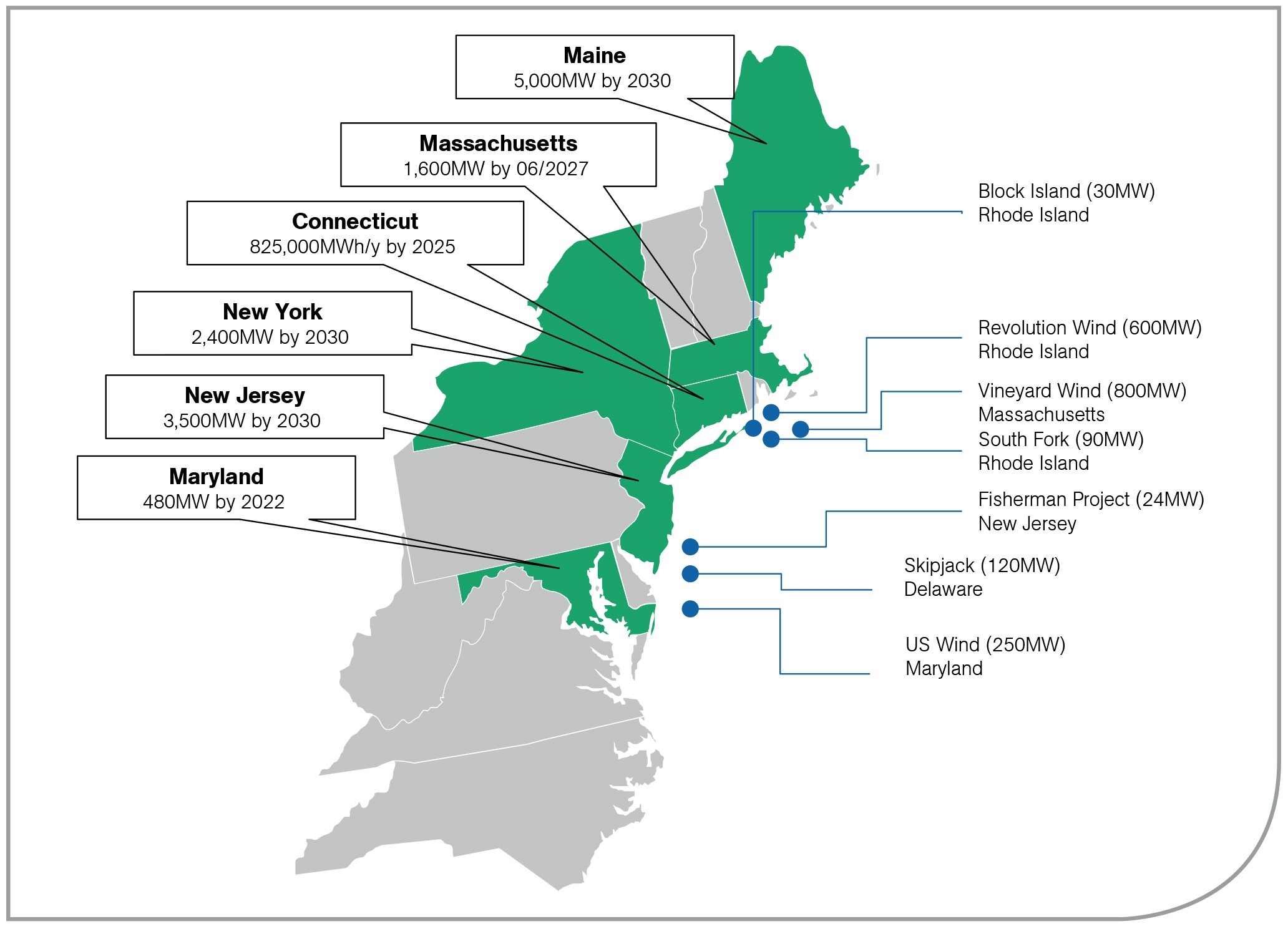

The first, and so far only, US offshore wind project was the modest-sized 30MW Deepwater Wind’s Block Island Wind project off the Rhode Island coast which was financed in 2015 and started up operations in late 2016. There have been no further US projects since then, but projects off the coasts of Massachusetts, Maryland, Rhode Island and Long Island, New York have been passing milestones that should lead to financial closings in 2019.

These states, along with New Jersey and Maine, all have ambitious goals for offshore wind capacity in the next decade.

The coming projects

In Maryland, two major projects are in development offshore Ocean City. The 750MW US Wind project would be built in phases with costs estimated at around $2.5 billion. Deepwater Wind’s Skipjack project would be a smaller $720 million project. The two projects have been awarded ocean renewable energy credits (OREC) purchase agreements in 2017 that would generate revenues at $167 per MWh for each project for 20 years, starting in 2021 for the US Wind project and at an inflating price in 2023 for Skipjack. US Wind has projected that it’s first 250MW phase would be completed in time for the OREC entitlement, so a financing is expected in the beginning of 2019.

In May this year, a Massachusetts-run procurement process settled on the 800MW Vineyard Wind Project proposed by a joint venture of Avangrid Renewables and Copenhagen Infrastructure Partners (CIP). The selection of the Vineyard Wind project allows the sponsors to go forward with negotiations for transmission services and PPAs. Permitting applications are in process to position this project for a construction start in late 2019 and operations in 2021.

At the same time, Rhode Island selected Deepwater Wind’s 400MW Revolution Project in a parallel procurement process that paves the way for the Revolution Wind developer to negotiate a services and power sales with National Grid that will ultimately be reviewed by the Rhode Island Public Utilities Commission. Deepwater hopes to be in a position to start construction in 2020 with start-up expected in 2023. Shortly after Rhode Island’s offshore wind award announcement, Connecticut also selected Deepwater’s Revolution Project to supply an incremental 200MW of wind energy to the state. Deepwater Wind will negotiate with two Connecticut electric distribution utilities, Eversource and United Illuminating, to reach agreement on 20-year contracts. If successful, the contracts will be brought to Connecticut’s Public Utility Regulatory Authority (PURA) for final approval.

In New York State, Deepwater Wind was awarded a 20-year PPA with the state-owned Long Island Power Authority (LIPA) for its 90MW South Fork project proposed for the south eastern shore of Long Island. Deepwater is currently working with the local town board on obtaining transmission easement rights and hopes to commence construction on its Long Island project in 2021, with start-up planned for 2022.

In New Jersey, the new Gov. Murphy administration has refocused on incentivizing offshore wind projects. Virginia is another mid-Atlantic state with ambitions for an offshore wind industry to take hold, and recently ran an RFP for consulting expertise to analyze maritime infrastructure and assets with the goal of informing the state’s policy related to the OSW industry.

European experience

While new to the US, offshore wind projects have been a regular source of investment and project finance activity in the European market for almost 20 years. The first offshore wind turbines were installed off the Danish and Dutch coast in the 1990’s by Denmark’s DONG Energy (now named Ørsted). The first utility-scale offshore wind installation was the 40MW Middelgrunden project in Danish waters in 2001. Offshore wind projects were increasingly deployed in the North Sea and Baltic waters throughout the first decade of the 21st century with capacity additions materially accelerating after 2010. Along the way, individual turbine sizes and capacities have continued to grow from the 1MW turbines employed in the earliest deployments to 3MW turbines and 5MW turbines by 2017, with latest turbines now approaching 12.5MW. Along with higher capacity factors, the offshore locations can accommodate larger turbine sizes. The technology has also advanced to permit deployment up to 60km offshore in waters 20-60 meters deep.

Asian markets, such as Taiwan, have also seen significant deployment in offshore wind, and lessons learned in prior European and Asian offshore wind project finance are likely to be brought to the upcoming round of US projects. Ørsted, CIP, and Avangrid arrive in the US market with a wealth of experience from their European developments while many of the leading project finance banks in the US already are institutionally quite experienced in financing offshore wind in other geographies.

Completion risk mitigation

The European experience indicates that completion risk will be a primary project finance issue. In the history of Europe’s build-out, completion delays and cost overruns presented challenges to early projects. In the first phase of utility-scale installations in the 2001-07 period, joint ventures of construction companies and marine companies would typically offer single turnkey equipment, procurement supply and installation contracts. However, many of these joint ventures absorbed material overrun costs, and the single turkey EPC became scarce in the early part of the present decade.

The completion risk made it impractical for developers to obtain the fixed-price turnkey contracts that have been the standard completion risk mitigation for onshore wind projects. Frequently, offshore wind projects were constructed on-balance sheet with project finance being introduced at the completion stage. Ørsted typically builds its projects using its own funding and recruits a financial partner that uses non-recourse finance for its investment.

While many developers elect to equity finance their projects during construction, non-recourse construction finance has also become available for offshore projects installed under the multi-contracting approach without a construction wrap. Multi-contracting involves sub-dividing the construction process into a number of manageable subcontracts. Typically, this involves a total of five to 10 contracts in areas such as civil works, turbine erection and substations. These would be coordinated by an experienced sponsor or owner’s engineer.

One advantage to this approach is it allows for area specialists with individually negotiated cost quotes, often leading to an overall lower cost compared to a fully-wrapped EPC contract.

A significant risk that arises under a multi-contracting or EPCI approach without a wrap is interface risk. In order to minimize this risk, developers generally seek to procure a limited number of EPCI contracts. For example, based on the European experience, projects have utilized three broad construction packages covering:

- turbine design, supply, installation and commissioning

- foundation design, supply, installation and commissioning

- balance of plant design, manufacturing, installation and commissioning, including interarray cables, foundations, and offshore substation platforms.

This approach achieves a good balance between limiting the number of contracts and selecting competent contractors for their relevant areas of expertise.

Leading European project finance banks have become comfortable with offshore construction arrangements without a wrap. These lenders closely examine the interface risks to ensure no contractual or physical gaps exist between contracts. Comfort is derived from sponsors that pro-actively manage the interfaces between contractors to assure the contracts are proceeding on the same project schedule. For such projects, lower leverage levels, well-sized contingency reserves and contingent equity have become routine for completion risk mitigation.

In the last few years, as the supply chain and installation techniques have become more flexible and reliable, some sponsors are now giving completion guarantees.

Ørsted’s £1.3 billion, 660MW Walney Project in 2017 was financed at competitive rates in consideration of the completion guarantee provided by that developer, and its 1,300MW Hornsea 1 financing is in the 2018 market also supported by the developer’s completion guarantee. However, other projects in the European market are still being financed under an EPCI approach.

What is not yet certain is whether EPCI contracts without a wrap will be required, or be found, for the early US offshore projects. Specialized shipping, rigs and the rest of the required marine infrastructure will need to be built out to enable the US offshore installations achieve the relatively lower costs and predictability of European marine construction projects now have.

Revenue support

The build-out of the European offshore wind industry has been subsidised by above-market revenues assured by long-term PPAs or RECs.

European tariffs have been declining in recent years, down from €200 per MWh for contracts awarded in the 2010-12 timeframe to more recent LCOE estimates in the €50-70 per MWh range.

The US’s only offshore wind project Block Island was supported by a PPA priced at $244 per MWh sourced before 2016, while the more recent contracts for the Ocean City and Skipjack projects have pricing starting at $167 per MWh in 2021.

Although these lower prices are due to the significant reduction in the cost of wind projects, they still represent a material increase over the wholesale power prices in these regional markets. The public policies adopted in the North Atlantic states aim to establish offshore wind as a job-generating industry so the early rounds of US offshore wind projects will likely benefit from above-market rates.

Capital sources

The US project finance debt market is already led by major European and Japanese banks that can import their global experience to finance the coming round of projects. Other US capital market participants, such as rating agencies and institutional investors, can be expected to catch up.

The other capital providers common to European projects are export credit agencies, particularly Denmark’s EKF which is regularly involved in offshore projects employing Vestas or Siemens equipment. Export credit agencies have only occasionally appeared in US project finance, but given the large amounts of capital to be raised among the upcoming US offshore wind projects, a place may be found for experienced debt providers who can hold large tickets.

A class of capital providers unique to the US renewables finance market have been the tax-equity sources: investors whose returns are largely met by tax-savings generated from the tax credits and accelerated depreciation that comes with renewables investments. The investment tax credit is scheduled to phase out in 2020, so this capital subsidy may not be available for projects beyond those that may be grandfathered by equipment purchased in 2018-19. However, if not properly managed, advance equipment/component purchases to grandfather tax benefits may be at odds with obtaining the latest and cheapest technologies.

The presence of tax-equity sources has made tax-equity bridge loans and back-leveraging partial partnership shares common features in US renewables finance, and they are expected to feature in early US offshore wind projects as well. Since tax-equity sources only become available once projects become operational, commercial banks are called upon to bridge the tax-equity commitments during the construction periods.

A US template

A template for structuring US offshore wind projects will likely emerge among the first of the upcoming projects drawing on the capital sources and elements unique to the US market, as well as the lessons learned in Europe and Asia. European developers and lenders are in the best position to set the standards for US offshore wind finance.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.