US upstream intention

Rebounding oil prices saw a surge in upstream oil & gas investments in the US last year (2017), but that enthusiasm may be more muted in 2018.

Global investment in upstream infrastructure is closely linked to the price of oil – not least shown in 2014-2015 with the activity by independent exploration and production (E&P) firms falling off in tandem with the downturn in oil prices.

The shale oil revolution in the US was a major contributor to the falling prices, creating an abundance of product and players in the market and cementing the country as a chief crude oil exporter with an average of 1.1 million barrels per day in 2017.

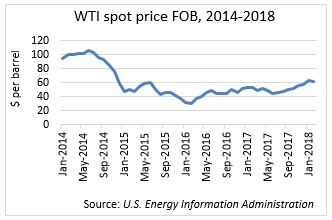

The West Texas Intermediate (WTI) price – settled at Cushing, Oklahoma – has demonstrated some level of stability in over the last two years, and in recent months it has risen to its highest level since late 2014.

Oil prices topped $65 per barrel in March (2018), and the positive trend has encouraged US E&P companies to embark on capital spending to increase their production capacities.

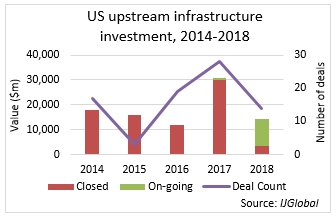

According to IJGlobal data, investments more than doubled in 2017 compared to previous years. The data includes primary financings on upstream infrastructure and M&A transactions in the sector. Much of the investment activity is focused on Eagle Ford Shale and the Permian Basin on the US Gulf Coast.

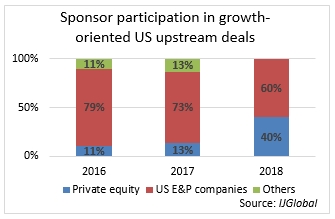

Beneficial market conditions are attracting private equity investors into US upstream. According to IJGlobal data, private equity accounted for 40% of upstream investment in the country in Q1 (2018).

However, while companies may be emboldened, there is some evidence that shareholders are still wary of another shale oil glut and subsequent downturn in price – Concho Resources’ share value dropped 8.8% after its $9.5 billion acquisition of RSP Permian was announced.

This may lead companies instead to opt for equity buybacks and divestments of non-core assets to improve shareholder returns and company value.

Another possible reason for caution is refinery capacity. Most existing refineries are still designed to handle heavier oils than shale, while 90% of the 3.1 million barrels per day increase in production between 2010 and 2017 has come from light tight oil (LTO).

According to the American Petroleum Institute, this has the potential to create a surplus of LTO reserves which could act as a brake on further price rises and potentially halt further upstream investment.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.