Questioning PABs

The private activity bonds (PABs) that financed a portion of the Indiana I-69 PPP were last week downgraded to junk (BB). The downgrade came as a result of construction delays, unresolved payment issues, and the financial deterioration of Isolux Corsan, parent of the project’s construction contractor.

The debt for Indiana 1-69 is now at risk of default, which has led some to call into question the use of tax-exempt bonds for US transport projects.

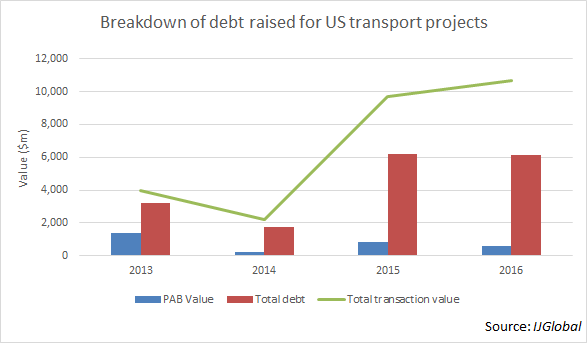

PABs provide a lower cost of funding for project sponsors and have been a mainstay in the US transport market in the last few years, often pricing out other commercial lenders. According to IJGlobal data, $3.1 billion of PABs have been issued for US transport projects in the past four years.

The value of PABs funding has increased since 2015. In 2016, to date, half of all US transport deals to reach financial close featured a PABs tranche. And roughly 10% of all debt on US transport deals that has reached financial close in 2016 was in the form of PABs.

The total value of PABs debt for 2016 so far is $585 million, according to IJGlobal data. However the majority of this total relates to the recently closed Maryland LRT transaction. The urban transit project was financed using $313.04 million of PABs. The remaining financing came in the form of an $874.6 million TIFIA loan, leaving no space for commercial lenders.

With PABs particularly vulnerable to construction delays, the problems suffered by the Indiana I-69 project could lead to greater scrutiny of their use.

Request a Demo

Interested in IJGlobal? Request a demo to discuss a trial with a member of our team. Talk to the team to explore the value of our asset and transaction databases, our market-leading news, league tables and much more.